Spirit AeroSystems Reports Second Quarter 2021 Results

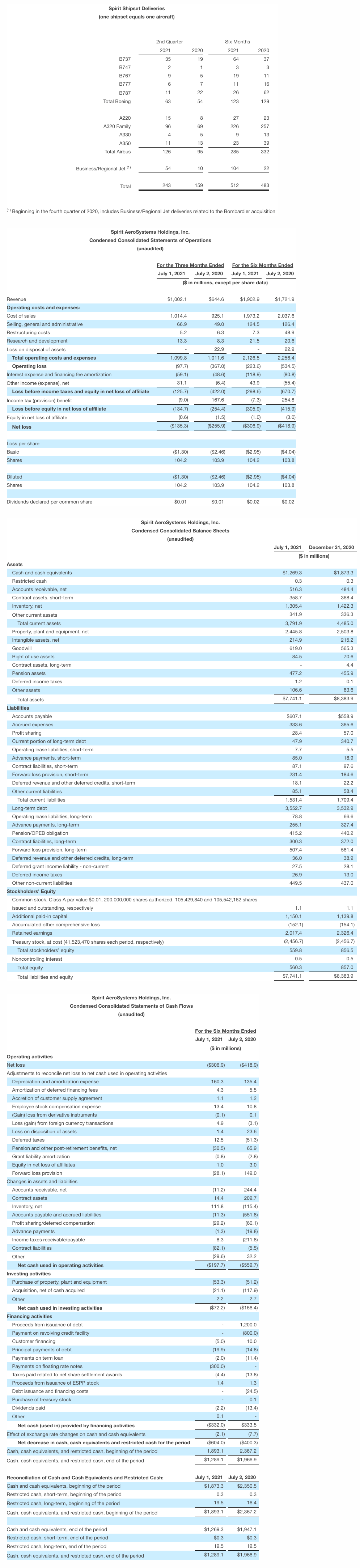

- Delivered 243 shipsets, compared to 159 in Q2 2020; delivered 35 737 shipsets in Q2 2021 compared to 19 in Q2 2020 and 29 in Q1 2021

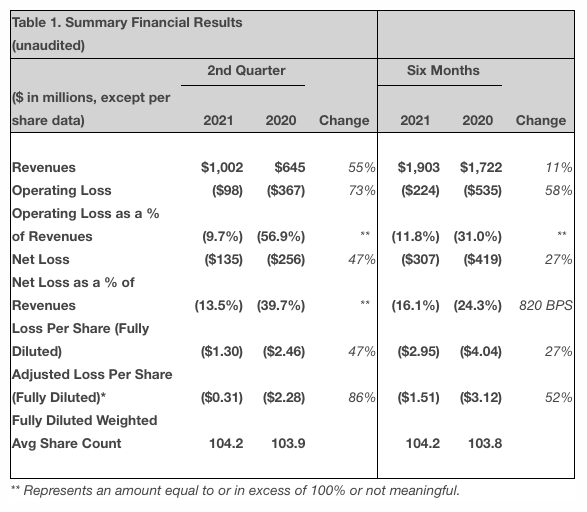

- Revenue of $1 billion in Q2 2021, compared to $645 million in Q2 2020 and $901 million in Q1 2021

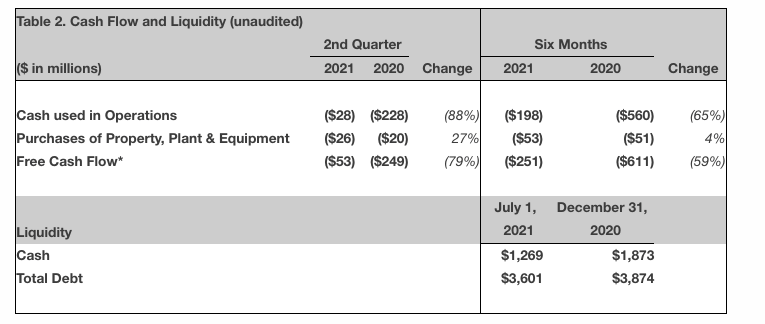

- Cash used in operations improved by $200 million from Q2 2020 and $142 million from Q1 2021

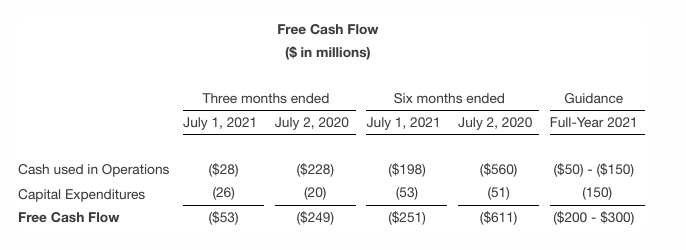

- Cash guidance unchanged: full-year 2021 cash used in operations is expected to be between $(50) to $(150) million; full-year 2021 free cash flow* is expected to be between $(200) and $(300) million

- EPS of $(1.30) in Q2 2021 compared to $(2.46) in Q2 2020; Adjusted EPS* of $(0.31) in Q2 2021 compared to $(2.28) in Q2 2020

WICHITA, Kan.--(BUSINESS WIRE)--Spirit AeroSystems Holdings, Inc. (NYSE: SPR) (“Spirit” or the “Company”) reported second quarter 2021 financial results.

“With continued improvement in domestic air traffic, we are seeing strong recovery in narrowbody production rates as compared to a year ago, which is leading to improved cash flow performance,” said Tom Gentile, Spirit AeroSystems President and Chief Executive Officer.

“As a result of our ongoing engagement with Boeing on the 787 program, we identified an additional issue in the forward section of the fuselage. We continue to coordinate with Boeing to ensure that we are performing all necessary rework. Primarily driven by this issue, we have recognized a $46 million forward loss on the 787 program in this quarter.”

Revenue

Spirit’s second quarter of 2021 revenue was $1.0 billion, up 55% from the same period of 2020, primarily due to higher production deliveries on the Boeing 737 and Airbus A320 programs and increased revenue from the recently acquired A220 wing and Bombardier programs. These increases were partially offset by the lower widebody production rates due to reduced international air traffic resulting from the impacts of COVID-19. Deliveries increased to 243 shipsets during the second quarter of 2021 compared to 159 shipsets in the same period of 2020, including Boeing 737 deliveries of 35 shipsets compared to 19 shipsets in the same period of the prior year.

Spirit’s backlog at the end of the second quarter of 2021 was approximately $34 billion, with work packages on all commercial platforms in the Boeing and Airbus backlog.

Earnings

Operating loss for the second quarter of 2021 was $97.7 million, as compared to operating loss of $367.0 million in the same period of 2020. The decreased loss was primarily driven by lower forward loss charges, lower costs related to excess capacity and lower losses on disposal of assets in the second quarter of 2021 compared to the second quarter of 2020. Second quarter 2021 earnings included $47.5 million of excess capacity costs and $9.9 million of favorable cumulative catch-up adjustments. Additionally, the second quarter of 2021 included net forward loss charges of $52.2 million, primarily driven by Boeing 787 engineering analysis and rework. In comparison, during the second quarter of 2020, Spirit recorded $194.1 million of net forward loss charges, excess capacity costs of $82.8 million and $37.7 million of unfavorable cumulative catch-up adjustments. Additionally, during the second quarter of 2020, Spirit recognized loss on disposal charges of $22.9 million related to certain long lived assets on the Boeing 787 and Airbus A350 programs.

Other income for the second quarter 2021 was $31.1 million, compared to a net expense of $6.4 million for the same period in the prior year. The increase primarily reflects income related to the Belfast pension plan during the second quarter of 2021, as well as a non-cash expense of $14.7 million recognized in the second quarter of 2020 resulting from the voluntary retirement program (VRP) offered during 2020 that did not recur in 2021.

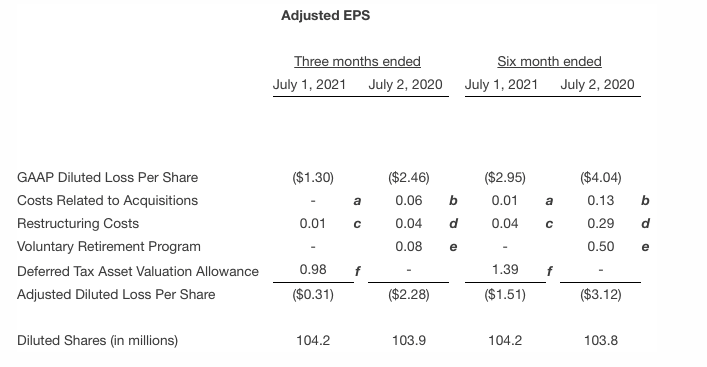

Second quarter EPS was $(1.30), compared to $(2.46) in the same period of 2020. Second quarter 2021 adjusted EPS* was $(0.31), which excluded the impacts from the acquisitions, restructuring costs and the incremental deferred tax asset valuation allowance. During the same period of 2020, adjusted EPS* was $(2.28), which excluded the impacts of planned acquisitions, restructuring costs and the VRP offered during the first quarter of 2020. (Table 1)

Cash

Cash used in operations in the second quarter of 2021 was $(28) million as compared to $(228) million in the same quarter last year, primarily due to positive impacts of working capital. Free cash flow* in the second quarter of 2021 was $(53) million as compared to $(249) million in the same period of 2020. The cash balance at the end of the second quarter of 2021 was $1.3 billion. (Table 2)

Financial Outlook and Risk to Future Financial Results – Unchanged August 4, 2021

Full-year 2021 cash used in operations is expected to be between $(50) and $(150) million; full-year 2021 free cash flow* is expected to be between $(200) and $(300) million.

Please refer to our Cautionary Statement Regarding Forward-Looking Statements below and the section captioned “Risk Factors” in the Company’s Annual Report on Form 10-K and the Company’s Quarterly Reports on Form 10-Q.

Subsequent Event

Based on the preliminary assessment of the latest 787 program demand received from Boeing on August 2, 2021, the Company expects to incur an incremental forward loss of approximately $40 to $60 million in the third quarter of 2021 due to the impact of reduced production volumes and the corresponding amount of fixed overhead absorption applied to lower deliveries. This preliminary assessment is subject to change if Boeing revises its production and delivery plans.

Segment Results

Fuselage Systems

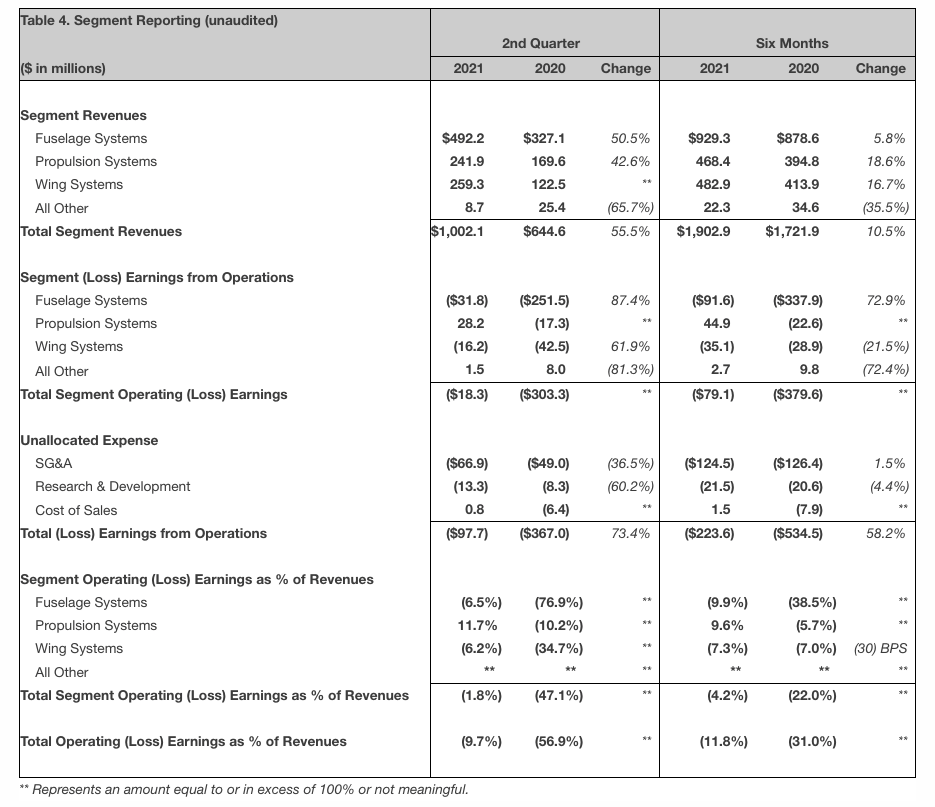

Fuselage Systems segment revenue in the second quarter of 2021 increased 51 percent from the same period last year to $492.2 million, primarily due to increased production volumes from the Boeing 737 and recently acquired Bombardier programs, partially offset by lower production volumes on the Boeing 787. Operating margin for the second quarter of 2021 increased to (6.5) percent, compared to (76.9) percent during the same period of 2020. This increase was primarily due to increased Boeing 737 production volumes and the resulting decrease in excess capacity costs, as well as less net forward losses recognized. In the second quarter of 2021, the Fuselage Systems Segment includes restructuring expenses of $0.9 million, excess capacity costs of $27.6 million and abnormal COVID-19 costs of $1.4 million compared to restructuring expenses of $2.4 million, excess capacity costs of $50.6 million, abnormal COVID-19 costs of $11.2 million, and loss on disposal charges of $22.5 million related to certain long lived assets on the Boeing 787 and Airbus A350 programs for the same period in 2020. In the second quarter of 2021, the segment recorded pretax $4 million of favorable cumulative catch-up adjustments and $35.7 million of net forward losses. In the second quarter of 2020, the segment recorded pretax $31.1 million of unfavorable cumulative catch-up adjustments and $155.1 million of net forward losses.

Propulsion Systems

Propulsion Systems segment revenue in the second quarter of 2021 increased 43 percent from the same period last year to $241.9 million, primarily due to increased revenue from the Boeing 737 program and aftermarket sales, partially offset by decreased production volume on the Boeing 777 program. Operating margin for the second quarter of 2021 increased to 11.7 percent, compared to (10.2) percent during the same period of 2020, primarily due to increased Boeing 737 production volumes and the resulting decrease in excess capacity costs, as well as lower net forward losses recognized compared to the same period of the prior year. In the second quarter of 2021, the segment recorded excess capacity costs of $7.1 million and $0.3 million of abnormal COVID-19 costs compared to excess capacity costs of $17.5 million, abnormal COVID-19 costs of $4.0 million and $1.6 million of restructuring expenses in the second quarter of 2020. The segment recorded pretax $5.9 million of favorable cumulative catch-up adjustments and $8.6 million of net forward losses in the second quarter of 2021. In comparison, during the same period of the prior year, the segment recorded pretax $5.1 million of unfavorable cumulative catch-up adjustments, and $16.2 million of net forward losses.

Wing Systems

Wing Systems segment revenue in the second quarter of 2021 increased significantly from $122.5 million in the same period last year to $259.3 million, primarily due to increased production deliveries on the Boeing 737, Airbus A320 and A220 programs. Operating margin for the second quarter of 2021 increased to (6.2) percent, compared to (34.7) percent during the same period of 2020, primarily due to increased Airbus A320 production volume as well as lower forward losses compared to the same period of 2020. In the second quarter of 2021, the segment includes $4.3 million of restructuring costs, excess capacity costs of $12.8 million and $0.7 million of abnormal COVID-19 costs compared to the same period the prior year, which included restructuring expenses of $2.3 million, excess capacity costs of $14.7 million and abnormal COVID-19 costs of $4.1 million. In the second quarter of 2021, the segment recorded pretax $0.4 million of unfavorable cumulative catch-up adjustments and $7.9 million of net forward losses. In the second quarter of 2020, the segment recorded pretax $1.6 million of unfavorable cumulative catch-up adjustments and $22.8 million of net forward losses.

Cautionary Statement Regarding Forward-Looking Statements

This press release contains “forward-looking statements” that may involve many risks and uncertainties. Forward-looking statements generally can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “could,” “continue,” “estimate,” “expect,” “goal,” “forecast,” “intend,” “may,” “might,” “model,” “objective,” “outlook,” “plan,” “potential,” “predict,” “project,” “seek,” “should,” “target,” “will,” “would,” and other similar words, or phrases, or the negative thereof, unless the context requires otherwise. These statements are based on circumstances as of the date on which the statements are made and they reflect management’s current views with respect to future events and are subject to risks and uncertainties, both known and unknown. Our actual results may vary materially from those anticipated in forward-looking statements. We caution investors not to place undue reliance on any forward-looking statements.

Important factors that could cause actual results to differ materially from those reflected in such forward-looking statements and that should be considered in evaluating our outlook include, but are not limited to, the following:

- the impact of the COVID-19 pandemic on our business and operations, including on the demand for our and our customers’ products and services, on trade and transport restrictions, on the global aerospace supply chain, on our ability to retain the skilled work force necessary for production and development, and generally on our ability to effectively manage the impacts of the COVID-19 pandemic on our business operations;

- demand for our products and services and the general effect of economic or geopolitical conditions, or other events, such as pandemics, in the industries and markets in which we operate in the U.S. and globally;

- the timing and conditions surrounding the full worldwide return to service (including receiving the remaining regulatory approvals) of the B737 MAX, future demand for the aircraft, and any residual impacts of the B737 MAX grounding on production rates for the aircraft;

- our reliance on Boeing and Airbus for a significant portion of our revenues;

- the business condition and liquidity of our customers and their ability to satisfy their contractual obligations to the Company;

- the certainty of our backlog, including the ability of customers to cancel or delay orders prior to shipment;

- our ability to accurately estimate and manage performance, cost, margins, and revenue under our contracts, and the potential for additional forward losses on new and maturing programs;

- our accounting estimates for revenue and costs for our contracts and potential changes to those estimates;

- our ability to continue to grow and diversify our business, execute our growth strategy, and secure replacement programs, including our ability to enter into profitable supply arrangements with additional customers;

- the outcome of non-conformance product warranty, defective product, or similar claims and the impact settlement of such claims may have on our accounting assumptions;

- our dependence on our suppliers, as well as the cost and availability of raw materials and purchased components;

- our ability and our suppliers’ ability to meet stringent delivery (including quality and timeliness) standards and accommodate changes in the build rates of aircraft;

- our ability to maintain continuing, uninterrupted production at our manufacturing facilities and our suppliers’ facilities;

- competitive conditions in the markets in which we operate, including in-sourcing by commercial aerospace original equipment manufacturers;

- our ability to successfully negotiate, or re-negotiate, future pricing under our supply agreements with Boeing, Airbus, and other customers;

- our ability to effectively integrate the acquisition of select assets of Bombardier along with other acquisitions that we pursue, and generate synergies and other cost savings therefrom, while avoiding unexpected costs, charges, expenses, and adverse changes to business relationships and business disruptions;

- the possibility that our cash flows may not be adequate for our additional capital needs;

- any reduction in our credit ratings;

- our ability to access the capital markets to fund our liquidity needs, and the costs and terms of any additional financing;

- our ability to avoid or recover from cyber or other security attacks and other operations disruptions;

- legislative or regulatory actions, both domestic and foreign, impacting our operations, including the effect of changes in tax laws and rates and our ability to accurately calculate and estimate the effect of such changes;

- our ability to recruit and retain a critical mass of highly skilled employees;

- our relationships with the unions representing many of our employees, including our ability to avoid labor disputes and work stoppages with respect to our union employees;

- spending by the U.S. and other governments on defense;

- pension plan assumptions and future contributions;

- the effectiveness of our internal control over financial reporting;

- the outcome or impact of ongoing or future litigation, arbitration, claims, and regulatory actions or investigations, including our exposure to potential product liability and warranty claims;

- adequacy of our insurance coverage;

- our ability to continue selling certain receivables through our supplier financing programs;

- and the risks of doing business internationally, including fluctuations in foreign currency exchange rates, impositions of tariffs or embargoes, trade restrictions, compliance with foreign laws, and domestic and foreign government policies.

These factors are not exhaustive and it is not possible for us to predict all factors that could cause actual results to differ materially from those reflected in our forward-looking statements. These factors speak only as of the date hereof, and new factors may emerge or changes to the foregoing factors may occur that could impact our business. As with any projection or forecast, these statements are inherently susceptible to uncertainty and changes in circumstances. Except to the extent required by law, we undertake no obligation to, and expressly disclaim any obligation to, publicly update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. You should review carefully the section captioned “Risk Factors” in the Company’s Annual Report on Form 10-K and the Company’s Quarterly Reports on Form 10-Q for a more complete discussion of these and other factors that may affect our business.

Appendix

In addition to reporting our financial information using U.S. Generally Accepted Accounting Principles (GAAP), management believes that certain non-GAAP measures (which are indicated by * in this report) provide investors with important perspectives into the company’s ongoing business performance. The non-GAAP measures we use in this report are (i) adjusted diluted earnings per share and (ii) free cash flow, which are described further below. The company does not intend for the information to be considered in isolation or as a substitute for the related GAAP measures. Other companies may define and calculate the measures differently than we do, limiting the usefulness of the measures for comparison with other companies.

Adjusted Diluted (Loss) Earnings Per Share. To provide additional transparency, we have disclosed non-GAAP adjusted diluted (loss) earnings per share (Adjusted EPS). This metric excludes various items that are not considered to be directly related to our operating performance. Management uses Adjusted EPS as a measure of business performance and we believe this information is useful in providing period-to-period comparisons of our results. The most comparable GAAP measure is diluted earnings per share.

Free Cash Flow. Free Cash Flow is defined as GAAP cash from operating activities (generally referred to herein as “cash used in operations”), less capital expenditures for property, plant and equipment. Management believes Free Cash Flow provides investors with an important perspective on the cash available for stockholders, debt repayments including capital leases, and acquisitions after making the capital investments required to support ongoing business operations and long term value creation. Free Cash Flow does not represent the residual cash flow available for discretionary expenditures as it excludes certain mandatory expenditures. The most comparable GAAP measure is cash provided by operating activities. Management uses Free Cash Flow as a measure to assess both business performance and overall liquidity.

The tables below provide reconciliations between the GAAP and non-GAAP measures.

|

a |

Represents the three and six months ended Q2 2021 transaction costs (included in SG&A) | |

|

b |

Represents the three and six months ended Q2 2020 transaction costs (included in SG&A) | |

|

c |

Represents the three and six months ended Q2 2021 restructuring expenses for cost-alignment and headcount reductions (included in Restructuring costs) | |

|

d |

Represents the three and six months ended Q2 2020 restructuring expenses for cost-alignment and headcount reductions (included in Restructuring costs) | |

|

e |

Represents the three and six months ended Q2 2020 retirement incentive expenses resulting from the VRP offered during the first quarter of 2020 (included in Other expense) | |

|

f |

Represents the three and six months ended Q2 2021 deferred tax asset valuation allowance (included in Income tax provision) |

* Non-GAAP financial measure, see Appendix for reconciliation

Contacts

Investor Relations: Ryan Avey or Aaron Hunt (316) 523-7040

Media: Molly Edwards (316) 523-2479

On the web: http:/ /www.spiritaero.com